Transaction Fraud Detection: A Comprehensive Guide for Security Leaders

Online transaction fraud poses a growing threat to businesses worldwide. Statista estimated that worldwide e-commerce losses from online payment fraud reached $44 billion in 2024.(1)

Fraudsters constantly adapt their techniques to exploit vulnerabilities in payment systems. From sophisticated bot attacks to malicious AI agents and advanced social engineering schemes, they leverage technology to commit fraud at an unprecedented scale. That’s why it’s more important than ever to protect your business against transaction fraud.

Key takeaways

- Transaction fraud occurs when attackers exploit stolen credentials or deceptive tactics to execute unauthorized payments.

- Fraudsters typically begin by gathering data through data theft or phishing, then validating it, and finally exploiting it.

- The rise of friendly fraud has contributed to increased chargeback rates in recent years.

- If your chargeback rate exceeds 1% of your total transactions, you need a dedicated fraud detection solution.

What is transaction fraud?

Transaction fraud happens when criminals use deceptive means to complete unauthorized financial transactions. Unlike traditional fraud, online transaction fraud primarily targets digital payment systems, e-commerce platforms, and mobile banking applications. To do so, it uses various techniques, from stolen credit cards to sophisticated identity theft schemes.

The digital nature of e-commerce has widened the scope of transaction fraud beyond simple unauthorized purchases. Sophisticated fraudsters use everything from payment processing vulnerabilities to account takeover techniques. This makes detection and payment fraud prevention difficult. A single successful attack can lead to substantial financial losses, a damaged reputation, and eroded customer trust.

And with 70% of consumers now using AI for shopping, e-commerce businesses must prepare for the emerging fraud risks that accompany agentic commerce.

According to DataDome’s 2025 Global Bot Security Report, 61.2% of websites are completely unprotected against basic bot attacks. As one of the most attacked industries globally, retail and e-commerce businesses remain highly exposed to carding, account takeover, and payment fraud.

How does transaction fraud work?

Online transaction fraud typically follows a systematic pattern that begins with gathering data. Fraudsters get payment information through stealing data, phishing for data, or buying data on the dark web. They often target large databases of customer information, where they look for credit card numbers, personal identification details, and login credentials.

Once criminals have the data, they move to the so-called validation phase. This is where they test stolen credentials with small purchases to check whether the credentials are valid. These “test transactions” are often automated with bots that can process thousands of attempts in a few minutes.

When a bot successfully validates a set of credentials, the fraudsters move to the exploitation phase. This is where they either make a larger purchase or sell the validated information to other criminals. In the first case, they will often then convert the stolen goods or services into cash by, for example, reselling it on legitimate marketplaces. They often also transfer their funds through multiple accounts, making the money trail harder to follow.

Why are chargeback rates going up?

As a business, you might have noticed that chargeback rates have gone up. This is for several interconnected reasons: The massive shift to digital payments has created more opportunities for fraudulent transactions. It’s also still hard to distinguish legitimate purchases from fraudulent ones. And consumer protection policies often favor the cardholder in disputes, making it easier for fraudsters to exploit the system.

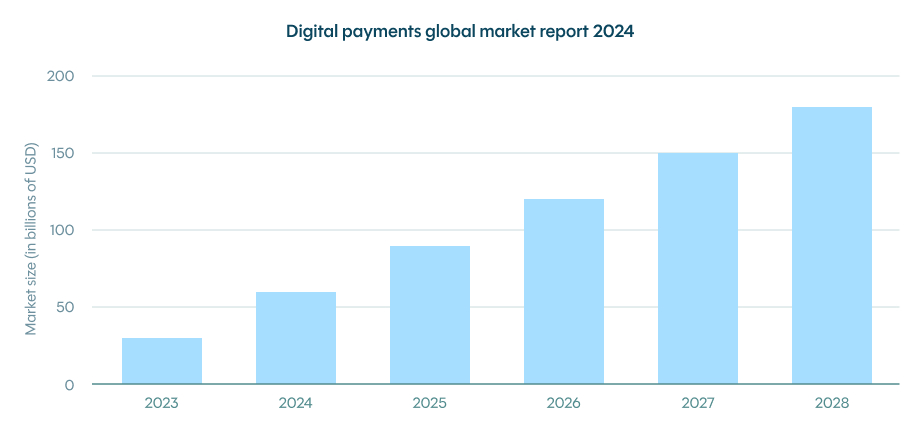

The value of digital payments is growing significantly every year

The rise of “friendly fraud” has also contributed to increased chargeback rates. “Friendly fraud” happens when legitimate customers dispute valid charges, either accidentally or intentionally. The phenomenon has become more common as consumers become more familiar with chargeback processes and sometimes abuse them for personal gain.

Another crucial factor is the increased sophistication of fraud rings that use automated tools. These criminal organizations use advanced technology to coordinate large-scale fraud operations, and often target multiple businesses simultaneously. Their use of residential proxies and sophisticated emulation tools makes their activities difficult to detect.

How can you know if you need transaction fraud detection?

The need for transaction fraud detection varies by business model and risk exposure. Companies that process a high volume of digital transactions face greater risks and typically need more robust protection. A key indicator is your chargeback rate: If it exceeds 1% of your total transactions, you need dedicated fraud detection solutions.

Industry type also plays an important role in determining your fraud risk levels. E-commerce businesses, digital goods providers, and companies that accept international payments face higher fraud risks due to the nature of their transactions. The same applies to businesses that offer same-day or express shipping options, as fraudsters often exploit rapid fulfillment to complete their schemes before you can detect them.

Beyond these immediate indicators, consider the potential impact of fraud on your business reputation and customer trust. Prevention typically costs less than dealing with the aftermath of fraud incidents, both in terms of direct financial losses and indirect costs like damaged customer relationships and brand reputation.

3 fundamental steps to detect transaction fraud

If you want to detect transaction fraud, you need a systematic approach that combines data collection, advanced analytics, and customized protective measures.

The following three fundamental steps are the foundation of a robust fraud detection strategy. By following these steps, you can build a comprehensive defense against fraudulent activities while maintaining a smooth customer experience.

1. Gather customer insights

A good understanding of how your customers typically behave is where it all starts. This begins by analyzing email addresses for suspicious indicators such as recently created accounts, disposable email services, or addresses linked to previous fraud attempts. Each transaction should be compared against known patterns of legitimate customer behavior.

Phone number verification serves as another important layer of authentication. By checking numbers against carrier databases and analyzing usage patterns, you can identify suspicious activities such as virtual numbers or numbers from high-risk regions. Legitimate customers typically maintain consistent phone numbers over time, while fraudsters frequently change their contact information.

Social and digital profiles provide additional verification layers. Most legitimate customers have established digital footprints across various platforms. The absence of social media profiles or online presence often indicates potential fraud, though this must be weighed against privacy-conscious customers who intentionally maintain a minimal online presence.

IP address monitoring helps identify suspicious patterns such as mismatches with billing addresses or the use of known proxy services. Multiple transactions from different cards using the same IP address often indicate fraudulent activity, as do rapid location changes that would be impossible for a legitimate customer.

Device fingerprinting tracks various characteristics to create unique identifiers for each customer’s device. This includes analyzing browser configurations, installed plugins, screen resolution, and other technical parameters that, when combined, create a distinctive profile that’s difficult for fraudsters to replicate.

2. Leverage machine learning insights

Modern fraud detection relies heavily on machine learning (ML) to analyze transaction patterns in real time and identify anomalies that might indicate fraud. These systems can process millions of data points simultaneously, adapting to new fraud patterns automatically while reducing false positives.

ML excels at identifying subtle patterns that human analysts might miss. For example, machine learning models can detect slight variations in typing patterns, mouse movements, or transaction timing that could indicate automated fraud attempts. These systems become more accurate over time as they learn from new data and fraud patterns. (More on ML in the next section.)

3. Create custom rules

Effective fraud prevention requires a combination of automated detection and customized rules based on your business’s specific requirements. These rules should reflect industry-specific fraud patterns, historical fraud data, and your business’s risk tolerance levels. Regularly review and update these rules to ensure they remain effective against evolving fraud tactics.

How is machine learning used in fraud prevention and detection?

Machine learning transforms fraud prevention through sophisticated pattern recognition across millions of transactions. It provides real-time risk scoring and behavioral analysis, and continuously adapts to new fraud patterns as they emerge.

Examples of machine learning for fraud detection

In-person payments represent one of the most established use cases for machine learning in fraud detection. ML systems analyze transaction patterns at physical terminals, identifying unusual purchase sequences or amounts that might indicate stolen cards. These systems can detect subtle patterns like rapid successive transactions at different locations or unusual spending patterns that deviate from a cardholder’s normal behavior.

Mobile payments present unique challenges that machine learning is particularly suited to address. ML algorithms analyze device fingerprints, location data, and user behavior patterns to identify potential fraud. The technology can detect when a device has been compromised or when transaction patterns suggest unauthorized access. Advanced systems even analyze how users interact with their devices, creating behavioral profiles that can spot imposters.

E-commerce fraud detection represents perhaps the most sophisticated application of machine learning. These systems analyze countless variables in real-time, from shopping cart composition to user navigation patterns. ML models can identify suspicious patterns like unusual shipping-billing address combinations, multiple failed payment attempts, or shopping behavior that doesn’t match typical customer patterns. The technology excels at detecting automated bot attacks that attempt to make purchases with stolen credit cards.

Other relevant use cases include peer-to-peer payment platforms, where machine learning analyzes transaction networks to identify suspicious patterns of fund movement. In cryptocurrency transactions, ML systems help detect money laundering patterns and fraudulent exchanges. For subscription services, these systems can identify potential subscription fraud by analyzing sign-up patterns and usage behavior.

Start detecting fraudulent transactions with DataDome

DataDome’s Cyberfraud Protection Platform defends your business across web, mobile, and API endpoints—combining advanced machine learning, real-time monitoring, and custom rules to stop transaction fraud before it impacts your bottom line.

The platform analyzes 5 trillion signals daily and processes each request in under 2 milliseconds, blocking fraudulent transactions while maintaining a seamless customer experience. With continuous threat intelligence updates and 24/7 expert support, DataDome keeps you protected against evolving fraud tactics.

In the case of PayPal, DataDome has ensured that cleaner traffic reaches core systems, fraud models work better, and fewer genuine users get falsely challenged—ultimately reducing operating costs by blocking unwanted traffic before it reaches PayPal’s infrastructure.

Don’t wait until fraud impacts your bottom line. Book a live product demo today to learn how our solution can protect your business from transaction fraud and other digital threats.

Transaction fraud FAQ

Most banks take 7-10 business days to refund fraudulent transactions after an investigation, though the exact timeline varies by financial institution. Some banks provide provisional credits within a few days while they investigate, but the permanent refund may take up to 90 days in complex cases.

Contact your bank or credit card issuer immediately to report the fraud and dispute the charge. Your bank will likely cancel your card, issue a new one, and start an investigation. Document the fraudulent charges and any evidence you have. Most financial institutions have zero liability policies for fraudulent charges when reported promptly.

When you report fraud, your financial institution typically cancels your compromised card, issues a new one, and opens an investigation. They’ll review the reported transactions, may ask you for additional information or documentation, and work to determine if fraud occurred. During this time, they may issue a provisional credit while they complete their investigation.

Filing a false fraud claim is a serious offense that can result in severe consequences, including criminal charges for fraud. Banks can close your accounts, report you to credit bureaus, and pursue legal action to recover funds. Additionally, merchants can provide evidence of legitimate transactions, leading to denied claims and potential penalties.

Key warning signs include multiple failed payment attempts, mismatched billing and shipping addresses, unusual order quantities or values, rush shipping requests on high-value orders, orders from high-risk countries, multiple orders using different cards from the same IP address, and transactions occurring at unusual hours or frequencies that don’t match typical customer behavior.

A chargeback rate above 1% is generally considered high and may trigger warnings from payment processors. Most card networks consider 0.9% the threshold for their monitoring programs. Rates above 2% can result in penalties, higher processing fees, or even account termination by payment processors and card networks.

Related posts

How Much Fraud Is Your Bot Vendor Missing? One Real-Money Gaming Platform Found Out the Hard Way

Tell me more

Libération Leverages DataDome + Arc XP to Neutralize Malicious AI Scraping in <2 Milliseconds

Tell me more

Etix Stops Ticket Scalping Without Slowing Down Real Fans

Tell me more

How to Prevent Credit Card Chargebacks: 9 Strategies to Protect Your Business

Tell me more